COLA's Role in Social Security and Inflation

Cost of Living Adjustments (COLA) might seem like just another bureaucratic term, but in reality, it holds a profound impact on millions of lives. As living costs rise due to inflation, COLA serves as a safeguard, ensuring that the benefits of retirees, particularly those from Social Security, maintain their purchasing power.

Inflation isn’t just about paying a few cents more for a loaf of bread. It reflects a wider economic picture where costs for crucial goods and services rise. For retirees who are on a fixed income, without COLA, they would find their purchasing power steadily eroding. This makes COLA an essential mechanism in ensuring that the real value of Social Security benefits doesn't diminish over time, even as market prices surge.

In the ever-changing landscape of financial security, understanding how COLA influences Social Security is essential. With inflation constantly shifting the value of our currency, it's imperative to know how COLA adapts to these changes to ensure beneficiaries receive fair benefits.

For those seeking further financial assistance or options, considering resources like social security disability loans can offer an added layer of support.

Origins and Importance of COLA

COLA originated as a response to the erosion of purchasing power due to inflation. Simply put, it's a method to ensure that the money people receive, especially on fixed incomes like pensions and social security benefits, retains its value over time. Without COLA, beneficiaries would find the real value of their benefits declining year after year. The adjustment is thus a safeguard, ensuring that the beneficiaries can maintain a consistent standard of living.

The calculation of COLA is not a simple task. It's determined using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which is a measure of the average change in prices over time of goods and services. Governing bodies monitor this index meticulously, using it as a benchmark to adjust benefits, ensuring they reflect current economic conditions.

How is the COLA Calculated?

When beneficiaries notice changes due to COLA, it spurs them to re-evaluate their financial plans. The $5000 social security loan frequently becomes a favored solution during these periods of fluctuation. But, what underlies these modifications? Here's an in-depth exploration:

- Initial Measurement Period: The average CPI-W for the third quarter (July, August, September) of the previous year is taken as a reference point.

- Comparison Period: This initial measurement is then compared with the average CPI-W for the third quarter of the current year.

- Determination of Percentage Change: The percentage change (increase or decrease) in the two averages gives the COLA for the next year. This ensures that if there's inflation (as indicated by an increase in the CPI-W), the benefits rise correspondingly. If there's deflation, benefits do not decrease.

- Application to Benefits: This derived percentage (like the 8.7% for 2023) is then applied to Social Security and Supplemental Security Income (SSI) benefits, effectively adjusting the amounts to counteract the effects of inflation.

These estimates give beneficiaries an idea of what to expect, helping them plan their finances more efficiently.

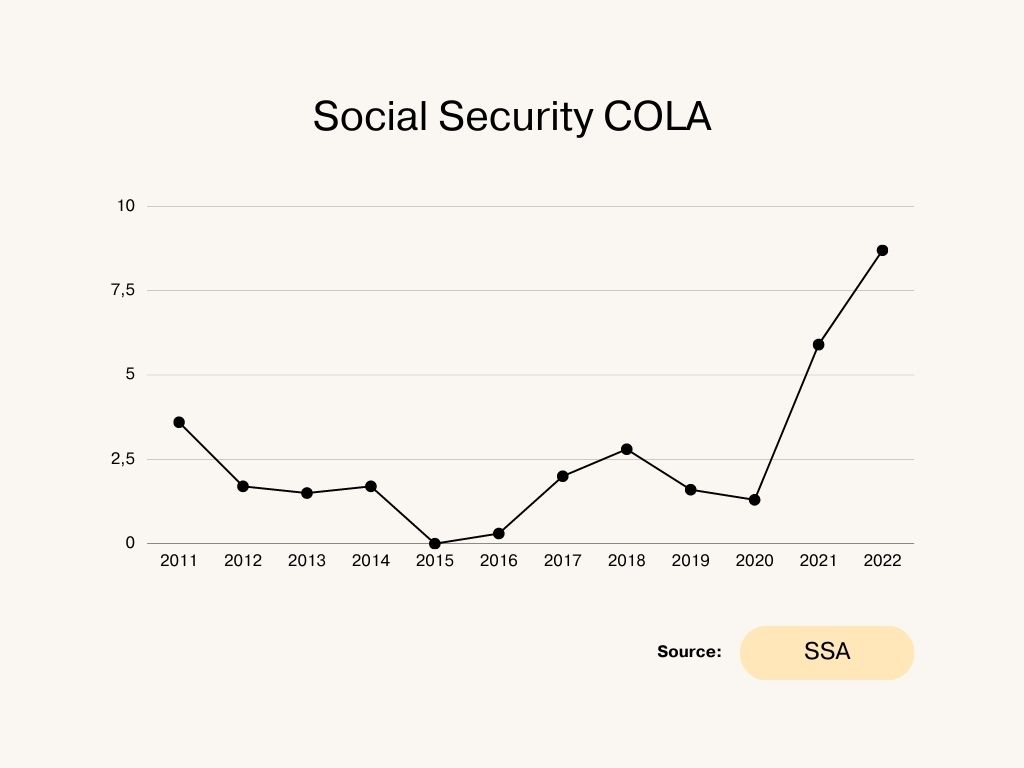

Social Secutity COLA by Year

The ebb and flow of COLA rates over the past ten years highlight the complexities of the global economy and domestic financial decisions. Several external and internal factors, ranging from geopolitical shifts to internal economic policies, played roles in influencing these numbers.

Analyzing the COLA across the years can provide insights into the economic environment of each year, and potentially predict future adjustments.

- Trend over the Years:

From 2011 to 2022, the COLA saw varied adjustments. The average COLA for these years is approximately 2.6%. However, the number alone does not paint the full picture. - Lowest Adjustments:

The years 2015 and 2016 witnessed the lowest adjustments at 0.0% and 0.3% respectively. A 0.0% adjustment indicates that the economic conditions did not necessitate an increase in the Social Security payments, likely due to low or negligible inflation. - Recent Surge:

Starting from 2021, there has been a noticeable increase in the COLA with 5.9% in 2021 and a further jump to 8.7% by the end of 2022. This is the highest adjustment in the given data set and might point to increased inflationary pressures or economic changes during these years. - Stable Period:

The period from 2012 to 2020 can be seen as relatively stable, with COLA mostly hovering between 1.3% and 2.8%. This suggests that during these years, inflation was relatively controlled, requiring only modest adjustments. - Legal Intervention:

The note on the 1999 COLA adjustment indicates that, originally, it was set at 2.4%. However, due to Public Law 106-554, it was effectively adjusted to 2.5%. This demonstrates that, at times, legal or policy changes can also influence the COLA beyond just economic factors.

2023 COLA Increase

For 2023, the Social Security Cost of Living Adjustment (COLA) has been established at an increase of 8.7 percent. The cost of living raise in 2023 had its own set of unique challenges and factors. Economic upheavals, along with policy changes, made it a significant year for adjustments. By understanding the intricacies of COLA 2023, beneficiaries and analysts can better predict and prepare for future trends.

This historical perspective doesn't just help beneficiaries. It provides policymakers with a foundation for future decisions, ensuring that Social Security recipients continue to receive benefits aligned with the cost of living.

Anticipating the Financial Future: A Look at COLA 2024

The landscape of COLA rates is a dynamic field, highly sensitive to a multitude of economic indicators. To understand the probable trajectory of COLA in 2024, it's essential to assess these pointers and the patterns they reveal.

Background

- After the previous two years saw the most significant Social Security COLAs in 40 years, 2024 anticipates a milder adjustment.

- The Social Security Administration (SSA) reported that the inflation metric, vital for determining the annual COLA, increased by 2.6% in July, setting the stage for the year's COLA determination.

Estimated COLA for 2024

- Expert Emerson Sprick from the Bipartisan Policy Center predicts a 3% COLA for 2024, translating to an approximate $55 monthly rise on the standard retirement benefit of $1,837 as of June 2023.

- This estimated increase is more conservative than the preceding two years, which stood at 5.9% and 8.7%, the highest since the early '80s.

June 2023 Inflation Data

- A 3% YoY inflation rate was reported, the lowest in over two years, largely propelled by housing and rental costs. This rate holds significance, especially for seniors relying on fixed incomes.

Projected COLA for 2024

- The Senior Citizens League uses the BLS data to forecast a 3% COLA for 2024, a slight rise from a previous 2.7% prediction. This figure may adjust based on forthcoming inflation figures from July, August, and September.

Implications for Beneficiaries

A 3% COLA would equate to an average monthly increment of about $53.60. Yet, the real impact on beneficiaries will be influenced by the Medicare Part B premiums for 2024, set to increase from $164.90 in 2023 to an estimated $174.80 in 2024.

New costs, like Medicare's coverage of the Alzheimer’s drug Lecanemab, could push this premium even higher, potentially to around $179.80/month.

A rise in benefits may also lead to heftier tax bills for some retirees, given that a segment of Social Security benefits may be taxable based on income levels. This scenario can adversely affect retirees as these taxation parameters haven't been inflation-adjusted since their implementation decades ago.

While the final figures for 2024 are pending, beneficiaries should be attentive to both the Social Security COLA and the Medicare Part B premium announcements. Furthermore, the inflation trajectory remains uncertain, influenced by various factors like potential wage growth and Federal Reserve decisions.

Recommendations for Retirees and Policymakers

Retirees stand at a unique crossroads with the COLA adjustments. It’s essential to reevaluate budgets, cut down on superfluous costs, and understand where every cent goes. For those tight months where the pension might not stretch enough, considering short-term solutions like payday loans with SSI debit card can be a stopgap, though it's crucial to use such options judiciously.

It’s never too late to invest wisely. With the COLA increase, retirees can explore diverse financial avenues, from bonds to savings accounts. It's about maximizing the return on every dollar, ensuring long-term financial stability.

The COLA determination process could benefit from being more transparent. Policymakers should look at offering clear rationales behind their decisions, ensuring retirees can anticipate and plan their finances better.

Engaging retirees in feedback sessions and understanding their challenges can lead to more empathetic and effective policies. It’s about refining the COLA process, ensuring it truly aligns with the retirees' needs and the nation's economic realities.

Breaking It Down: What 2024 Might Bring

As we approach 2024, there's a lot of talk about COLA (Cost of Living Adjustments). These adjustments matter because they affect how much money retirees get from Social Security. Here’s a breakdown of what we know and why it's important:

- The 2024 COLA Increase: Current predictions suggest that Social Security checks might increase due to COLA in 2024. This means retirees might get more money each month.

- Comparing Predictions: When we look at different expert opinions, there’s a general agreement that retirees can expect some changes in their monthly funds.

- Wider Impact: It's not just about Social Security. Changes in COLA can influence things like federal worker pay, disability rates, and military salaries. So, this is a change that can touch various parts of society.

- Planning is Key: For retirees, these potential changes highlight the importance of financial planning. On a bigger scale, the country's economy, stock markets, and even government budgets will have to adjust to these shifts.

For retirees, it's essential to stay informed and make plans based on the expected changes. For those making the policies, the goal is to ensure that these adjustments are done right and benefit everyone.

In short, as we gear up for 2024, everyone should be prepared for the financial changes on the horizon. Being proactive and informed will help both individuals and the nation navigate the adjustments smoothly.

You are about to post a question on compacom.com:

Any comments or reviews made on this website are only individual opinions of the readers and followers of the website. The website and its authors team are not responsible, nor will be held liable, for anything anyone says or writes in the comments. Further, the author is not liable for its’ readers’ statements nor the laws which they may break in the USA or their state through their comments’ content, implication, and intent.